As we step into a new year with a fresh start, it’s the perfect time to review and enhance your financial strategy. One integral aspect that deserves your attention is tax planning. This comprehensive guide will explore effective tax planning strategies to optimize your financial position and minimize tax liabilities. Let’s delve into strategic tax planning for a prosperous year ahead.

The Importance of Strategic Tax Planning

Strategic tax planning is not merely about complying with tax regulations; it’s also about optimizing your financial decisions to minimize tax burdens. A proactive approach allows you to keep more of your hard-earned money and strategically allocate resources for wealth while giving enough to Uncle Sam.

Aligning Your Financial Goals with Tax Objectives

Begin the new year with a clear understanding of your financial goals. Whether saving for retirement, funding education, or building wealth, it’s essential to understand what you want to accomplish to best align these goals with tax planning strategies to maximize benefits and minimize tax implications.

Staying Informed about Tax Law Changes

Tax laws evolve, and staying informed is crucial. Keep abreast of new tax regulations or changes that may impact your financial situation. Being proactive in understanding these changes ensures you can adapt your tax planning strategies accordingly. We’ll discuss a few of those evolving regulations below.

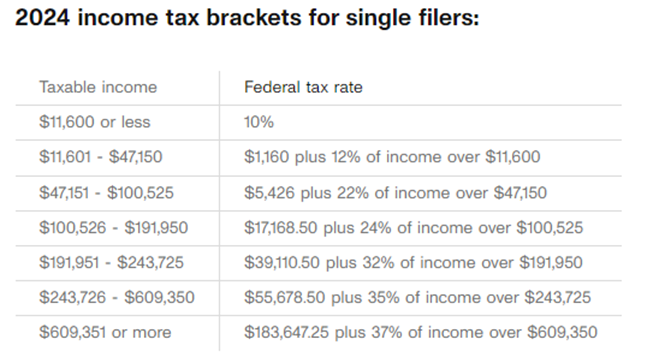

2024 Federal Income Tax Brackets

The IRS is raising federal income tax brackets in 2024. With this change, you might fall into a lower tax bracket than you did the year before. For example, if Maddie, a single filer, made $45,000 in 2023, she would have fallen into the 22% tax bracket for the year. If Maddie’s income remains at $45,000 in 2024, she would fall in the 12% tax bracket. This means that Maddie will pay less federal tax in 2024 than in 2023 and will have less money withdrawn from her paycheck.

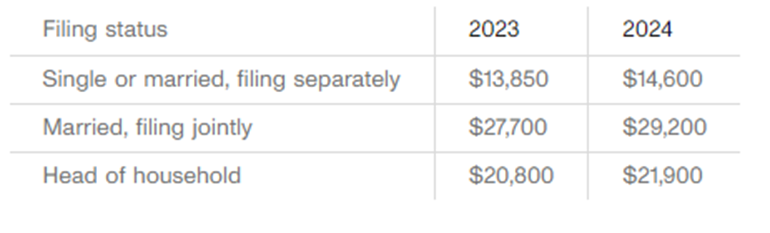

2024 Standard Deduction

The standard deduction is a specific dollar amount that tax filers may subtract from their income before income tax is applied. The alternative to the standard deduction is itemized deductions, expenses that can be deducted from your adjusted gross income to reduce your tax bill. It makes sense to take the itemized deduction if the total cost exceeds the standard deduction (more on itemized deductions below).

Source for all charts: IRS (PDF)

Social Security Changes

If you collect Social Security, you will receive a 3.2% cost-of-living adjustment in 2024. Since the first of January falls on a holiday, you have likely already received your first increased SSI payment at the end of December.

Tax Credits and Adjustments

A tax credit is a tax incentive that allows certain taxpayers to subtract the amount of credit they have accrued from their total tax due. Unlike tax deductions, tax credits reduce the amount of tax owing rather than taxable income. Check out the tax credits on the IRS website to determine which credits are available.

Strategies for Strategic Tax Planning

Let’s explore actionable strategies to incorporate into your tax planning arsenal for the new year.

Optimizing Tax-Advantaged Accounts

- Maximizing Contributions to Retirement Accounts:

- Pre-tax retirement accounts, like 401(k)s and Traditional IRAs, are great ways to defer taxes and save for your future. The deduction limit for 401(k) contributions in 2024 has increased from $22,500 to $23,000. Bonus: If you are over 50, you can contribute an additional $7,500 for a total of $30,500.

- The deduction limit for Traditional and Roth IRAs in 2024 increased from $6,500 in 2023 to $7,000. You can contribute an additional $1,000 for $8,000 if you are 50 or older.

- Exploring Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs):

- Leverage HSAs and FSAs for healthcare expenses. Contributions to these accounts are tax-deductible, providing a strategic way to manage medical costs while enjoying tax benefits. Review the differences between HSAs and FSAs to determine which account is best for you and your family.

- 529 Accounts:

- If you have children, grandchildren, or a favorite niece, consider setting up a 529 plan. Starting in 2024, you can contribute up to $18,000 per donor per beneficiary to qualify for an annual gift tax exclusion. Contributions may be deductible depending on your state, plus earnings are tax-free when used for qualified education expenses.

Strategically Timing Income and Deductions

- Income Deferral and Acceleration:

- Evaluate your income sources and consider deferring or accelerating them based on your current and future tax situations. Strategic timing can impact your taxable income in a way that minimizes your overall tax liability.

- Itemizing Deductions:

- Assess whether itemizing deductions makes sense for your financial situation. Deductible expenses such as mortgage interest, medical expenses, and charitable contributions can significantly reduce your taxable income. It makes sense to elect to itemize your deductions if the total amount of deductions is more significant than the Standard Deduction (discussed above).

Tax-Efficient Investment Strategies

- Harvesting Capital Gains and Losses:

- Evaluate your investment portfolio and consider capital gain and loss harvesting. This strategy involves selling investments to offset gains with losses, minimizing your overall tax liability. Speak with a tax professional to see if this strategy applies to you every year.

- Utilizing Tax-Efficient Investments:

- Explore investments with tax advantages, such as tax-efficient mutual funds or tax-managed portfolios. These options can help you optimize your after-tax returns.

- Charitable Contributions:

- If you’re charitably inclined, most taxpayers can generally deduct any charitable donations up to 50% of their taxable income. Another option to consider is gifting a stock that has high capital gains. Instead of selling the position and possibly incurring a sizeable taxable gain, you can give that stock to your favorite charity.

Incorporating Tax Planning into Your New Year Plan

Setting Clear Objectives and Milestones

As you embark on the new year, integrate tax planning into your financial plan. Set clear objectives and milestones, ensuring your tax planning strategies align with your broader financial goals.

Regularly Reviewing and Adjusting Strategies

Financial landscapes change, and so should your tax planning strategies. Regularly review your financial situation and adjust your tax planning strategies to accommodate any life changes, market shifts, or regulatory updates.

Consulting with Tax Professionals

Enlist the expertise of tax professionals to navigate complex tax scenarios. Their insights can uncover additional opportunities for tax savings and ensure compliance with the latest tax laws.

Strategic tax planning is the cornerstone of financial success. As you embark on a new year, integrate these tax planning strategies into your financial plan to maximize wealth accumulation and minimize tax liabilities. Stay proactive, stay informed, and make tax planning an integral part of your financial journey.

Remember, a well-executed tax plan saves you money and empowers you to achieve your financial goals and live the life you want for yourself. Here’s to a financially savvy and prosperous new year plan! If you’re interested in learning more about how to plan for your taxes, please contact our team here at ML&R Wealth Management.